Discom’s poor financial health still remains a challenge for large scale deployment in India..

The recently released report of IEA “Renewables 2021” highlights that the poor financial health of Discoms and piling outstandings of solar and wind developers is becoming a major hurdle in further deployment of renewables.. With current installation of renewables capacity of about 70 GW, it is expected that we add yet another 120 GW renewables installations by 2026. Discom’s poor financial health is becoming challenge..

- The Discoms overdue payments are piling to the tune of Rs. 1200 billion, Which is close to about 12% of their outstanding payments. The recent capital infusion to Discoms, led to faster payments by Discoms, however the conditions in 2021 has become at the same level and there no sign of improvement. THough GOI has announced a new stimulus program of USD 41 Billion, however the focus is to reduce the distribution losses through smart metering and other infrastructure support. The non payment to solar and wind developers still remains a challenge.

- The recently introduced basic custom duty and supply chain challenges has led to 40% reduced capacity deployment in 2020, and we expect the similar outcome in 2021 as well. This will surely lead to missing the GOI ambitious target of 175 GW renewables by 2022, 500 GW by 2050, and net zero targets by 2070.

- The poor financial health of Discoms is leading to renegotiation downwards the solar and wind PPAs. About 12 GW of solar capacity awarded pre Covid times as a part of manufacturer linked solar capacity is facing the implementation challenges due to the offtakers are not signing the PPAs. The Andhrapradesh also cancelled its 6.4 GW solar auction due to disputed contract rules.

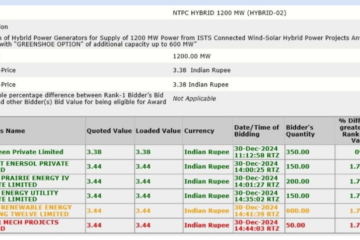

- Equipment cost inflation in solar and wind projects is now clearly visible in recent price bids, and implications of introduction of BCD of 40% will take the solar tariffs upwards. The local content requirements will now allow the solar panel prices to come down in short tterm until we are becoming self sufficient in our manufacturing capacity.

- Rising electricity prices to domestic and industrial consumers will still attract the distributed/rooftop solar installations. However the netmetering hurdles beyond 10 kW solar installation will hamper the growth targets of distributed solar as well.