Introduction: The Invisible Border Tax

Over the past five years, India has exported over ₹65,000 crore worth of iron and steel products to the European Union. This isn’t just a trade corridor—it’s a carbon corridor. Now, the European Union’s Carbon Border Adjustment Mechanism (CBAM) threatens to flip the script.

What was once a margin-based game is now a mandate-based market. The CBAM essentially transforms the EU’s internal carbon pricing (under ETS) into an external tariff on high-carbon imports, starting 2026. And Indian steelmakers are standing directly in the crosshairs.

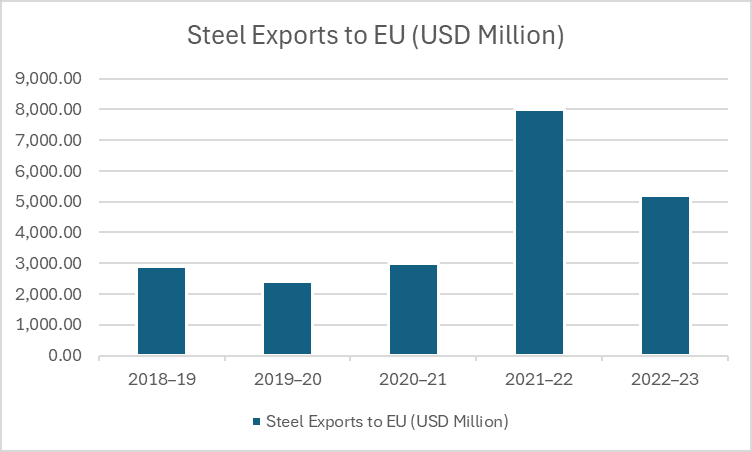

The Growth Boom: Steel Exports to EU

Over FY2018–FY2023, India’s iron and steel exports to the EU surged, peaking at $8 billion (₹60,000 crore+) in FY22. This reflected both global recovery and strong demand for semi-finished and long steel products.

Figure 1: India’s Steel Exports to EU (2018–2023)

The Carbon Cost Curve: ₹9,000 Cr Liability by 2034

What’s lurking beneath these export numbers is the carbon cost. Under CBAM, each tonne of steel exported to the EU will attract a carbon tariff aligned with EU ETS prices. At current intensity levels, Indian BF-BOF steel producers could face a CBAM surcharge of $4.36/tonne, rising as EU phases out free allowances.

CBAM Exposure = A New Trade Barrier

- EU’s free allowance phase-out begins in 2026 and ends by 2034

- For Indian steel exporters, this means:

- ₹190 Cr liability in 2026

- ₹9,048 Cr liability in 2034 (zero allowances)

- All without a single change in customs duty

- Table: Estimated CBAM Liability (INR Cr):

| Year | Free Allowance (%) | CBAM Liability |

| 2026 | 97.5% | ₹190 Cr |

| 2028 | 90.0% | ₹794 Cr |

| 2030 | 51.5% | ₹4,019 Cr |

| 2034 | 0.0% | ₹9,048 Cr |

From Legacy to Leap: Why Indian Steel Must Transition

India’s steel sector is dominated by the BF-BOF route—highly carbon-intensive. The future belongs to DRI–EAF using green hydrogen, where emissions fall below 0.5 tCO₂/tonne. This isn’t just climate compliance—it’s cost advantage.

🔍 India’s Comparative Emission Profile:

- India (BF-BOF): ~2.5 tCO₂/ton

- EU (EAF): ~1.3 tCO₂/ton

- Green DRI-EAF (Future): ~0.3–0.5 tCO₂/ton

Exporters who don’t switch face automatic margin erosion. In a green steel world, carbon is currency.

A National Green Steel Mission?

If India can build a ₹1.4 lakh crore PLI scheme for electronics and semiconductors, why not a national Green Steel Export Competitiveness Mission?

This must include:

- Mandatory MRV systems for Scope 1+2 emissions

- Green hydrogen procurement corridors

- Carbon price pass-through models in export contracts

- A carbon registry linked to India’s upcoming Carbon Credit Trading Scheme (CCTS)

Final Word: Go Green or Go Home

CBAM is not a trade war—it’s a carbon adjustment. For India’s steelmakers, this is a reset moment. The EU isn’t asking for less steel—it’s asking for cleaner steel. With over ₹65,000 Cr already at stake, this is not a climate story—it’s an economic survival plan.