If carbon markets were judged by outcomes instead of intentions, the EU ETS would be Exhibit A in climate misdirection.”

The European Union’s Emissions Trading System (EU ETS), once hailed as the flagship of global carbon pricing, is failing to deliver on its most urgent promise: industrial decarbonisation.

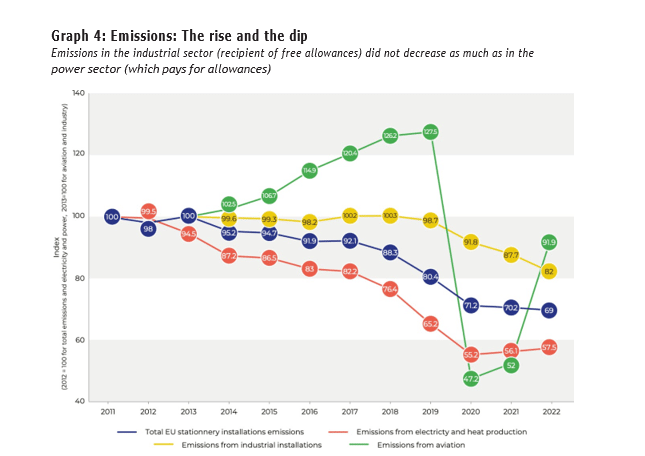

While power sector emissions in the EU have dropped, the dirtiest industries — cement, aluminium, steel, and aviation — continue to pollute with little consequence. The reason is as simple as it is inconvenient: free allowances.

Power Sector vs Industry: A Tale of Two Systems

- Between 2013 and 2019, industrial sector emissions fell by a meagre 1.3%.

- In the aviation sector, emissions increased during the same period.

- In contrast, power sector emissions dropped by 27% between 2005 and 2016 — thanks in part to auctioned permits and renewable deployment.

So while the power sector paid for its emissions, industry got a free ride.

95% Free: Carbon Without a Cost

The failure is embedded in the system design. Up to 95% of all EU Allowances (EUAs) issued to industry were given for free, effectively neutralising any carbon price signal.

In economic terms, this means zero incentive to innovate. Why decarbonise when the cost of pollution is nil?

The same industries are now being protected again — this time by shifting the cost of decarbonisation onto exporters through CBAM.

Carbon Price Theatre

ETS prices are currently in the €80–€100/tCO₂ range. But this market signal is a mirage unless all sectors are equally exposed.

While power producers paid up, steel, aluminium and aviation players banked free allowances, passed on hypothetical costs to consumers, and reported climate compliance — without cutting emissions.

CBAM is now being sold as a “levelling mechanism,” but in truth, it is a late-stage patch for a rigged system.

The False Equivalence of Emission Reduction

Let’s be clear: Emission reduction in the EU over the last 15 years has come not from ETS enforcement but from:

- Renewables driven by feed-in tariffs and mandates

- Fuel switching, particularly from coal to gas

- Deindustrialisation, especially post-2008

ETS was not the cause, but the beneficiary of these trends.

What This Means for India and the Global South

CBAM assumes that pricing carbon equals reducing carbon. But the EU’s own experience shows otherwise.

Now, Indian steelmakers, aluminium smelters, and cement producers will be asked to pay a carbon price Europe’s own industries never paid.

The Global South must prepare not just to defend against carbon tariffs, but to redefine decarbonisation beyond the price tag.